Investment Analysis of Banking Sector in Nepal

Analysis of Investment Opportunities in Nepal's Banking Sector

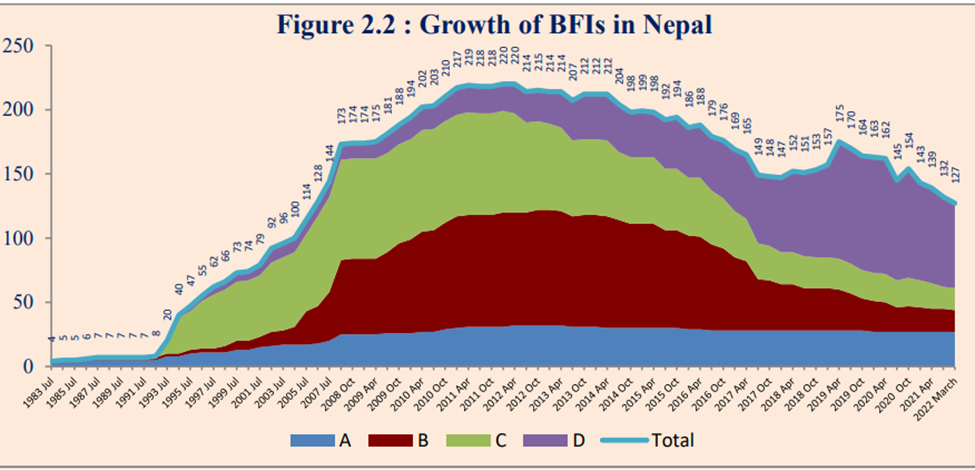

Transformation of the Banking Sector in Nepal

The modern banking system in Nepal traces its roots back to 1937 with the establishment of Nepal Bank Limited. Initially, it operated as the sole financial institution in the country until the Nepal Rastra Bank (NRB) was established in 1956. In the 1960s, two government-owned banks were established, further diversifying the banking landscape. However, significant development and diversification of the financial system began in the mid-1980s.

Financial liberalization in the 1980s opened the doors for increased private sector involvement in the banking industry. This led to a surge in the number of financial institutions, reaching a total of 220 by 2012. Joint venture banks introduced technological advancements to the industry, contributing to the expansion of financial access and inclusion.

In recent years, there has been a growing focus on consolidating the financial sector. The global financial crisis of 2007-08 prompted central banks worldwide to prioritize the strengthening of capital foundations and risk management practices. Nepal followed suit, and since the implementation of the merger bylaw in 2011, there has been an increase in merger and acquisition activities in the banking sector.

By 2012, there were 220 financial institutions in Nepal, including 32 commercial banks, 88 development banks, 77 finance companies, and 23 microfinance institutions (MFIs). The monetary policy of 2015/16 played a pivotal role in encouraging merger and acquisition practices by requiring A, B, and C class financial institutions to increase their paid-up capital fourfold. Consequently, the number of banks and financial institutions gradually decreased. As of mid-March 2022, Nepal has 27 commercial banks, 17 development banks, 17 finance companies, 66 MFIs, and one infrastructure development bank.

Recent Debate on Financial Consolidation in Nepal

There has been a debate among academics and policymakers regarding the success of the financial consolidation movement in achieving its objectives. One argument suggests that bank mergers have led to increased efficiency in the banking sector and reduced the cost of financial services. Proponents of this view also argue that mergers have enhanced the resilience of banks. On the other hand, an equally strong counterargument suggests that bank mergers have limited competition in the banking sector and go against market principles.

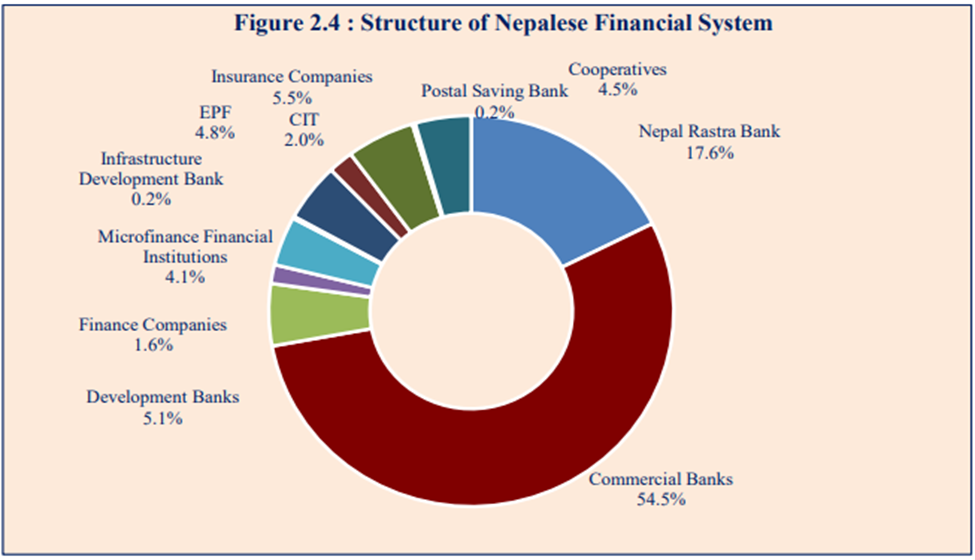

Structure of the Nepalese Financial System

The financial system in Nepal consists of deposit-taking and contractual saving institutions. Deposit-taking institutions include commercial banks, development banks, finance companies, and microfinance institutions (MFIs). Other financial institutions include insurance companies, employee's provident fund, citizen investment trust, postal saving offices, cooperatives, non-government organizations performing limited banking activities, and the Nepal Stock Exchange. The central bank of Nepal, the Nepal Rastra Bank (NRB), regulates the banking sector, which includes commercial banks, development banks, finance companies, and MFIs.

As of mid-March 2022, there are 27 commercial banks, 17 development banks, 17 finance companies, 66 MFIs, and 1 infrastructure development bank licensed by the NRB. Commercial banks constitute the largest part of the financial system, accounting for 54.5 percent of the assets, followed by the NRB with 17.6 percent. Development banks, finance companies, and MFIs represent 5.1 percent, 1.6 percent, and 4.1 percent of the system's assets, respectively. On the non-bank side, insurance companies hold a share of 5.5 percent, while cooperatives account for 4.5 percent.

Merger Guidelines and Regulatory Framework

The Nepal Rastra Bank (NRB) has implemented various regulatory provisions to facilitate the merger and acquisition of banks and financial institutions (BFIs). The NRB introduced the merger bylaw in 2011, which was subsequently amended in 2012. Additionally, the acquisition bylaw was enacted in 2013. To streamline these regulations, the NRB integrated the two bylaws into the merger and acquisition bylaw of 2016. This bylaw has undergone continuous amendments to further facilitate mergers among BFIs.

The primary objectives of the existing bylaws are as follows:

- Enhancing the credibility of BFIs in the public domain by promoting the overall banking and financial system.

- Maintaining financial stability by ensuring good governance, security, and the effectiveness of the country's banking and financial system.

- Developing the competitive capacity of the financial system by improving its capital base.

- Providing modern, high-quality, and reliable banking services to the public by promoting financial, human resource, technical, and other capacities.

- Safeguarding the interests of depositors, borrowers, and other stakeholders.

Source: Nepal Rastra Bank

Importance of the Banking Sector in Nepal's Underdeveloped Economy

The banking sector holds significant importance in an underdeveloped country like Nepal due to the following reasons:

Financial Inclusion: In Nepal, a considerable portion of the population, especially in rural and remote areas, lacks access to banking services. The banking sector has the potential to promote financial inclusion by expanding its reach to underserved communities. By providing essential financial services such as savings accounts, credit facilities, and remittance services, banks can empower individuals, support small enterprises, alleviate poverty, and address existing financial disparities.

Mobilizing Savings and Investments: Banks play a crucial role in gathering savings from individuals and enterprises. By offering secure and reliable deposit facilities, banks encourage people to save their funds instead of keeping them idle. These accumulated savings can be channeled into investments across various sectors such as agriculture, infrastructure, tourism, and manufacturing, thereby stimulating economic growth and progress.

Access to Credit: Availability of credit is vital for fostering entrepreneurship, business growth, and economic activities. In Nepal, where access to financial resources is limited, the banking sector plays a crucial role in providing loans and credit to individuals and enterprises. This enables them to make investments that generate income, create employment opportunities, and contribute to overall economic development.

Remittance Management: Remittances from Nepali migrant workers abroad form a significant source of income for many households in Nepal. The banking sector plays a pivotal role in effectively managing and directing these remittances. By providing remittance services, facilitating international money transfers, and offering tailored financial solutions, banks contribute to financial stability, promote efficient utilization of remittances, and drive economic growth.

Infrastructure Development: Nepal requires substantial infrastructure development to support economic growth. Banks provide crucial financial support for infrastructure projects, including roads, bridges, hydropower plants, and telecommunications networks. Through long-term loans, project financing, and investment capital, banks contribute to infrastructure development, which in turn stimulates economic activities and improves the quality of life for the population.

Risk Management and Financial Stability: The banking sector plays a vital role in managing and minimizing financial risks, ensuring the stability of Nepal's financial system. By evaluating borrowers' creditworthiness, monitoring risks, and establishing robust risk management frameworks, banks foster trust in the economy, attract domestic and foreign investments, and promote sustainable economic growth.

Employment Generation: The banking sector is a significant contributor to employment opportunities in Nepal. It offers a wide range of jobs in finance, accounting, customer service, technology, and other fields. The sector's growth creates employment opportunities, reduces unemployment rates.

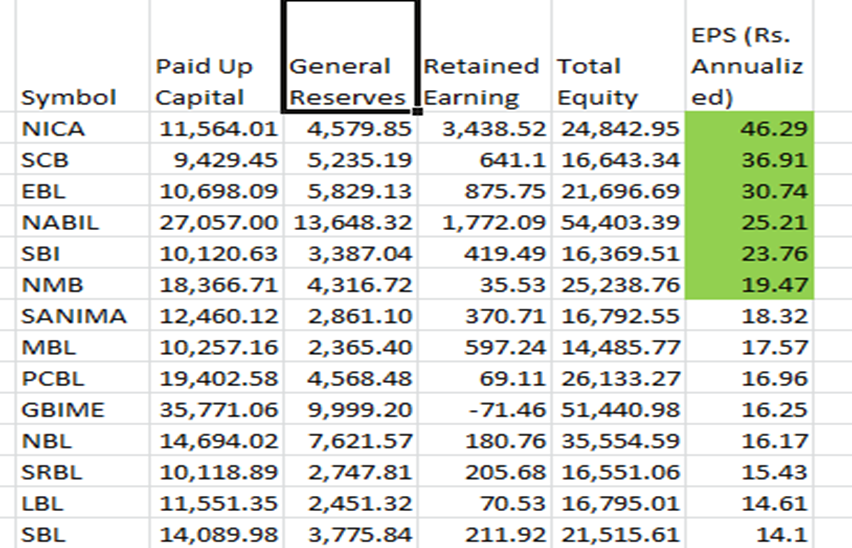

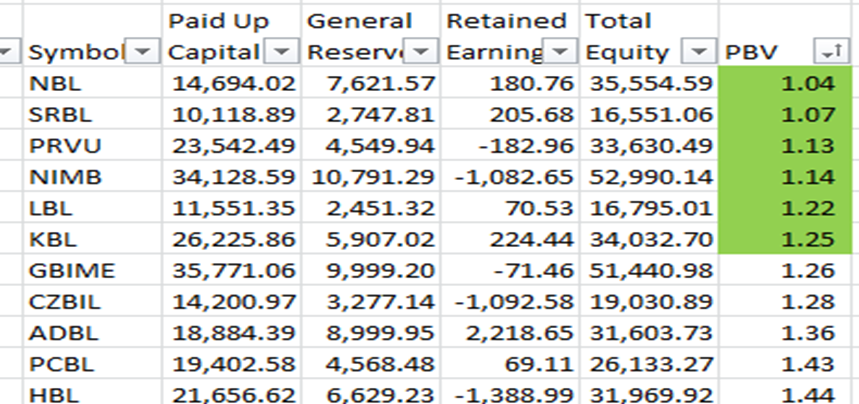

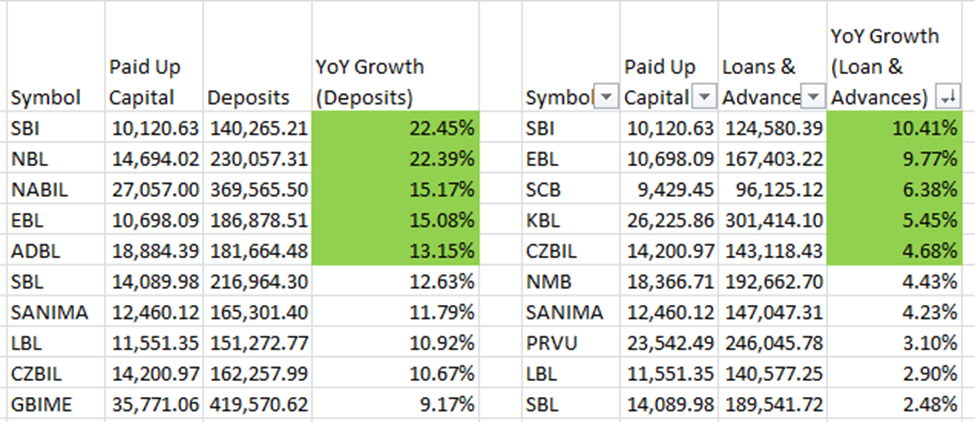

When making investment decisions, it is recommended to prioritize banks with higher earnings per share (EPS). Furthermore, considering banks with lower price-to-earnings ratio (PE) and price-to-book value (PBV) is prudent. By considering these factors, investors can make more informed choices about their investments. Additionally, the growth of deposits and loans in the banking sector is another important factor to consider. As a bank's deposits increase, its ability to provide loans expands, leading to growth in its loan portfolio and increased profitability. Similarly, when loans expand, banks experience a corresponding increase in profitability.

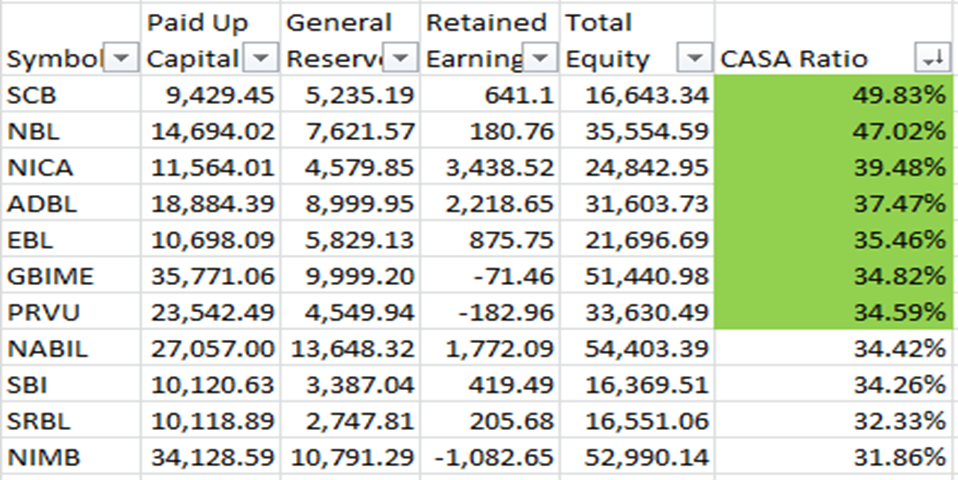

Likewise, the Current Account Savings Account (CASA) ratio is a metric used in the banking industry to measure the percentage of a bank's deposits that originate from current accounts and savings accounts. Current accounts are non-interest-bearing accounts commonly used by individuals and businesses for regular transactions such as receiving salaries and paying bills. On the other hand, savings accounts are designed to earn interest on deposited funds and are primarily intended for saving money. A higher CASA ratio is generally considered beneficial for a bank as it indicates lower funding costs and improved profitability. This ratio suggests that the bank has a significant portion of its deposits in current and savings accounts, which are typically more stable and less expensive compared to other funding sources. It is important to note that CASA ratios can vary among banks and can be influenced by factors such as the bank's customer base, product offerings, and marketing strategies. As a result, the specific CASA ratios for each bank can exhibit significant variations.

t's important to note that investing in the banking sector, like any investment, carries inherent risks. Factors such as economic conditions, regulatory changes, credit quality, and operational risks can impact the performance of banking stocks. Conducting thorough research, assessing the financial health of banks, and seeking professional advice can help investors make informed investment decisions in the banking sector in Nepal. Trading in the banking sector Investors who adopt a more conservative approach may find trading in stocks with a beta value of less than 1 to be an intriguing strategy. A beta value below 1 indicates that the stock typically exhibits less volatility compared to the overall market. The banking sector companies in the Nepse, in particular, have notably low beta values. Consequently, the price fluctuations in this sector tend to be minimal in comparison to other sectors in the Nepse. To assist with trading in such stocks, here are a few important factors to bear in mind: 1. Stocks with a beta value below 1 are known for their stability and are anticipated to have relatively smaller price fluctuations when compared to the overall market. This characteristic often appeals to investors who adopt a more conservative investment approach. 2. In periods of market downturns, stocks with a beta value below 1 typically exhibit a relatively smaller decline compared to the broader market. This characteristic can offer a degree of safeguarding to your investment portfolio during volatile market conditions. 3. Stocks with beta values below 1 are commonly associated with well-established companies that distribute dividends. For investors seeking to generate income from dividends, directing attention towards stocks exhibiting a beta less than 1 may prove advantageous. Hence, when considering trading opportunities, it is imperative to focus on volatile stocks whose prices exhibit significant fluctuations within short periods. Traders seek to capitalize on these price movements by strategically buying low and selling high, or vice versa, within condensed timeframes. However, it should be noted that the banking sector, characterized by high market capitalization and abundant shares, tends to be less volatile compared to other sectors with lower market capitalization and limited share supply. Consequently, the banking sector may not be as suitable for traders since the manipulation of company shares is less likely. Nonetheless, from a risk management perspective, trading within the banking sector offers an advantage due to its high volume and liquidity. This ensures that traders can easily find buyers and sellers, facilitating prompt entry and exit from positions with minimal impact on prices. It is crucial to acknowledge that engaging in stock trading entails a higher level of risk in contrast to long-term investing. Active trading requires diligent analysis, ongoing monitoring, and the capability to promptly respond to evolving market circumstances. Prior to embarking on active trading, it is advisable to possess a comprehensive comprehension of technical and fundamental analysis, proficient risk management strategies, and access to dependable market data. Furthermore, seeking guidance from a financial expert or seasoned trader can furnish valuable insights to facilitate trading endeavors. Key Business model The key business model of the banking sector in Nepal is based on providing a range of financial services to individuals, businesses, and institutions. Here are the key elements of the banking business model in Nepal: Core Banking Services: Banks in Nepal offer core banking services, which include accepting deposits, providing loans and credit facilities, and facilitating domestic and international payment transactions. These services form the foundation of the banking business model and generate a significant portion of the banks' revenue. Interest Income: Banks earn interest income by lending money to borrowers. They provide various types of loans, including personal loans, business loans, housing loans, and agricultural loans. The interest charged on these loans forms a major source of revenue for banks in Nepal. Fee-based Services: Banks generate additional income through fee-based services. This includes charges for account maintenance, remittances, debit and credit card services, ATM usage, and other transactional services. Fee income diversifies the revenue streams and supplements the interest income. Investment and Treasury Operations: Banks in Nepal engage in investment and treasury operations to optimize their capital and generate returns. They invest in various financial instruments, such as government securities, corporate bonds, and equities. Treasury operations involve managing the bank's liquidity, foreign exchange transactions, and hedging activities. Trade Finance and Foreign Exchange: Nepal's banking sector provides trade finance services to facilitate international trade transactions. Banks issue letters of credit, provide export and import financing, and offer foreign exchange services. Trade finance and foreign exchange operations contribute to the banks' revenue and support cross-border transactions. Retail Banking and Wealth Management: Banks in Nepal focus on retail banking, serving individual customers with products such as savings accounts, fixed deposits, and consumer loans. They also provide wealth management services to high-net-worth individuals, offering investment advisory, portfolio management, and customized financial solutions. Digital Banking and Innovation: With the increasing adoption of digital technologies, banks in Nepal are embracing digital banking channels and services. They offer online banking, mobile banking, and other digital platforms to enhance customer experience, improve accessibility, and streamline banking operations. Risk Management and Compliance: Banks prioritize risk management and compliance to ensure the safety and soundness of their operations. They employ risk management frameworks, credit assessment processes, and internal controls to manage credit, liquidity, operational, and regulatory risks. Branch Network and Customer Relationships: Banks in Nepal maintain an extensive branch network to provide convenient access to their services. Branches serve as customer touch points, facilitating account opening, customer inquiries, and personalized banking services. Building strong customer relationships and delivering quality service is a critical aspect of the banking business model. It's important to note that individual banks may have specific strategies and variations within this business model based on their size, target market, and competitive positioning. Adaptation to evolving customer preferences, regulatory changes, and technological advancements is key for banks to remain competitive and sustain their business model in the dynamic banking landscape of Nepal. Qualitative analysis using SWOT analysis SWOT analysis is a framework used to assess the strengths, weaknesses, opportunities, and threats of a specific industry or organization. Here's a SWOT analysis of the Nepalese banking sector: Strengths: Stable and Resilient: The Nepalese banking sector has demonstrated stability and resilience, even during challenging times. It has weathered various economic and political uncertainties, showcasing its ability to withstand external shocks. Growing Economy: Nepal's economy has been growing steadily, offering opportunities for banks to expand their operations and benefit from increased demand for financial services. Sound Regulatory Framework: The banking sector operates under a robust regulatory framework governed by the Nepal Rastra Bank (NRB). The NRB's regulations promote transparency, risk management, and financial stability, contributing to the sector's overall strength. Increasing Financial Inclusion: The banking sector has made strides in promoting financial inclusion by expanding its reach to underserved areas and population segments. This provides opportunities for banks to tap into previously untapped markets. Weaknesses: Limited Penetration in Rural Areas: While progress has been made in financial inclusion, there is still limited banking penetration in rural and remote areas of Nepal. This poses a challenge for banks in reaching a significant portion of the population. Limited Product Diversification: The banking sector in Nepal is relatively concentrated, with a limited range of product offerings. There is scope for banks to diversify their product portfolios to cater to evolving customer needs and preferences. Opportunities: Infrastructure Development: Nepal presents significant opportunities for infrastructure development. Banks can play a crucial role in financing infrastructure projects, including roads, hydropower plants, and tourism-related infrastructure, contributing to economic growth and expanding their lending portfolios. Digital Banking: There is potential for banks to leverage digital technologies to enhance their services and reach a wider customer base. Embracing digital banking solutions can increase operational efficiency, improve customer experience, and tap into the growing digital-savvy population. Threats: Competition from Non-Bank Financial Institutions: Non-bank financial institutions, such as microfinance institutions and cooperatives, pose competition to traditional banks. These institutions cater to specific customer segments and may offer innovative financial products and services. Economic and Political Risks: Nepal faces inherent economic and political risks that can impact the banking sector. Factors such as policy changes, political instability, and external economic shocks can affect the sector's performance. Asset Quality Risks: Ensuring sound credit quality and managing non-performing loans is crucial for banks. Inadequate risk management practices and economic downturns can lead to increased default risks and negatively impact the financial health of banks. It's important to note that this SWOT analysis provides a general overview and that the actual strengths, weaknesses, opportunities, and threats may vary for individual banks within the Nepalese banking sector. Guidelines issued by the NRB that could potentially affect the profitability of the banking sector. The guidelines issued by the Nepal Rastra Bank (NRB), the central bank of Nepal, can have various impacts on the profitability of commercial banks in the country. Here are some ways in which NRB guidelines can affect commercial banking profitability: 1. Interest Rate Policies: The NRB sets benchmark interest rates and provide guidelines on lending and deposit rates. Changes in these interest rate policies can directly impact the profitability of commercial banks. For example, NRB could decide to increase or decrease the spread rate which could potentially increase the interest on loan. Spread rates: The net interest rate spread is the difference between the average yield a financial institution receives from loans and other interest-accruing activities and the average rate it pays on deposits and borrowings. Interbank rate: It is an interest rate at which banks borrow and lend their funds in the money market for short term. It is an overnight lending of one bank to another. Base rate: Base rate refers to the minimum standard rate below which the commercial banks are not allowed to lend. In other words, the base rates is the cost of doing the banking business. Base rate includes Base Rate calculation is done by taking majorly five factors into consideration. - the cost of deposits - the administrative costs borne by the bank - the cost of reserve maintained by the Bank with the Central Bank - the opportunity cost of cash held by the bank - and other fixed assets. However, for the time being, the cost of fixed assets has been halted by Nepal Rastra Bank for being included in the calculation of the Base Rate. In the review of monetary policy, it was announced that the spread rate of commercial banks will be reduced from 4.4 percent to 4 percent for commercial banks and development banks and finance companies should apply 4.6 percent spread rate. When banks will maintain the spread rate as per the instructions of NRB by the third quarter and that will reduce the interest rate of loans. As the banks have reduced the interest rate on deposits since January, the cost of capital was decreased in April, and the base rate was also decreased. 2. Capital Adequacy Requirements: The NRB imposes capital adequacy requirements on banks to ensure they maintain sufficient capital to absorb potential losses and maintain financial stability. Banks may need to raise additional capital to meet these requirements, which can increase their costs and potentially reduce profitability. CAR represents a banks capacity to meets its time liabilities and others risk such as Credit risk and operational risk. The Basel III norms stipulated a capital to risk weighted assets of 8.5%. However, as per NRB norms, Nepal scheduled commercial banks are required to maintain a CAR of 11%. Tier 1 Capital means which can absorb the loss without a bank require stopping its trading activities. Tier 2 Capital means which can absorb the loss in the event of dissolution CAR = (Tier 1 capital + Tier 2 Capital)/ Risk weighted assets Where, Tier 1 capital = (paid up+ Statutory reserve + Disclosed free reserve – Equity investment in subsidiaries + intangible assets + current and brought forward losses Tier 2 Capital = (undisclosed reserves + general loss reserve + hybrid debt capital instruments & subordinated debt) In accordance with the guidelines set by the Nepal Rastra Bank (NRB), it is of utmost importance for banks to uphold a Tier 1 Capital of 8.5% and a Tier 2 Capital of 11% on a quarterly basis. Failure to meet these stipulations will result in the bank being unable to declare dividends for the respective financial year, and may lead to penalties imposed by the NRB. 3. Reserve Requirements: The NRB sets reserve requirements, including cash reserve requirements (CRR) and statutory liquidity ratio (SLR), which determine the portion of deposits that banks must hold as reserves. These requirements can impact banks' liquidity position and their ability to deploy funds for lending or other profit-generating activities. Increasing reserve requirements of CRR and SLR will increase the Base rates of Bank. While decreasing it decreases the base rates of bank. The Cash Reserve Ratio (CRR), which is the minimum cash that BFIs must maintain as deposit at NRB, has been increased from 3% to 4% of the total deposit base of a bank in monetary policy of 2079/80. Similarly, the Statutory Liquidity Ratio (SLR), which is the minimum liquid assets that BFIs much hold as government security, has been increased to 12% for commercial banks and 10% for development banks and financial institution in monetary policy of 2079/80. 4. Loan Classification and Provisioning: The NRB provides guidelines on loan classification and provisioning, requiring banks to set aside reserves for potential loan losses. Stricter guidelines in this area can increase the amount of provisions banks need to make, impacting their profitability. 5. Risk Management: The NRB may issue guidelines on risk management practices that banks must adhere to. Compliance with these guidelines can require additional investments in risk management systems and processes, which can impact profitability. 6. Governance and Compliance: The NRB may issue guidelines on governance practices and regulatory compliance measures that banks must follow. Ensuring compliance with these guidelines may involve additional costs related to implementing compliance systems, conducting audits, and staff training. 7. Technology and Digital Banking: The NRB may issue guidelines to regulate and promote secure digital transactions, customer data privacy, and cyber security in the banking sector. Banks may need to invest in technology infrastructure and security measures to comply with these guidelines, which can impact profitability.

When the reserve requirements for the Cash Reserve Ratio (CRR) and Statutory Liquidity Ratio (SLR) increase, it leads to a corresponding increase in banks' base rates. Conversely, reducing these reserve requirements results in a decrease in base rates. These adjustments in reserve requirements play a significant role in influencing banks' base rates, which in turn impact the costs of borrowing and lending in the financial system.

The Credit-to-Core-Capital plus Deposit (CCD) ratio has been replaced by the Credit-Deposit (CD) ratio. The CCD ratio used to indicate a Banking and Financial Institution's (BFI) ability to convert deposits and core capital into loans, while the CD ratio focuses solely on the ability to cover loans using deposits. According to new regulations, BFIs are required to maintain a CD ratio of 90%, which is an increase from the previous CCD ratio of 85%. It's important to note that the CD ratio should not exceed 90% until mid-July 2022. This adjustment has resulted in a decrease of available loan funds in the overall banking and finance system by an estimated 400-500 billion.

Nonperforming loans (NPLs) refer to loans where borrowers have defaulted and have not made the required payments of principal or interest for a specified period. In the banking sector, commercial loans are classified as nonperforming when the borrower is 90 days overdue. As per regulations set by the National Regulatory Body (NRB), commercial banks are prohibited from

declaring dividends for a specific financial year if their nonperforming loans exceed 5%.

Incentives are provided to commercial banks involved in mergers and acquisitions until mid-July 2023. A discount of 1% is available on the SLR and 0.5% on the CRR for one year of integrated transactions. The institutional fixed deposit limit and individual institution's deposit will be increased by 5%. The cooling period of 6 months will not apply to the board of directors and senior officers of such commercial banks. The spread rate can exceed up to 1% of the permissible limit of 4.4%. If the loan-deposit ratio exceeds the limit in integrated transactions, a one-year period will be given to manage it.

The Reverse Repo Rate is a tool used by the NRB to control inflation by absorbing liquidity from the market. It is the interest rate at which the NRB borrows money from commercial banks. The Reverse Repo Rate allows the NRB to obtain funds from commercial banks when needed by offering them an attractive interest rate. The term "REPO" refers to a repurchase option or agreement, which is a monetary tool allowing commercial banks to borrow money from the NRB against collaterals such as government bonds and treasury bills. When lending money to commercial banks, the NRB charges an interest rate known as the repo rate.

It is important to note that the specific impact of NRB guidelines on commercial banking profitability can vary depending on factors such as individual bank's financial health and business strategies. Additionally, changes in NRB guidelines can have both positive and negative effects on profitability, depending on the specific circumstances.

The financial analysis area

Symbol

Paid Up Capital

General Reserves

Retained Earning

Total Equity

CASA Ratio

EBL

10,698.09

5,829.13

875.75

21,696.69

35.46%

SBI

10,120.63

3,387.04

419.49

16,369.51

34.26%

SCB

9,429.45

5,235.19

641.1

16,643.34

49.83%

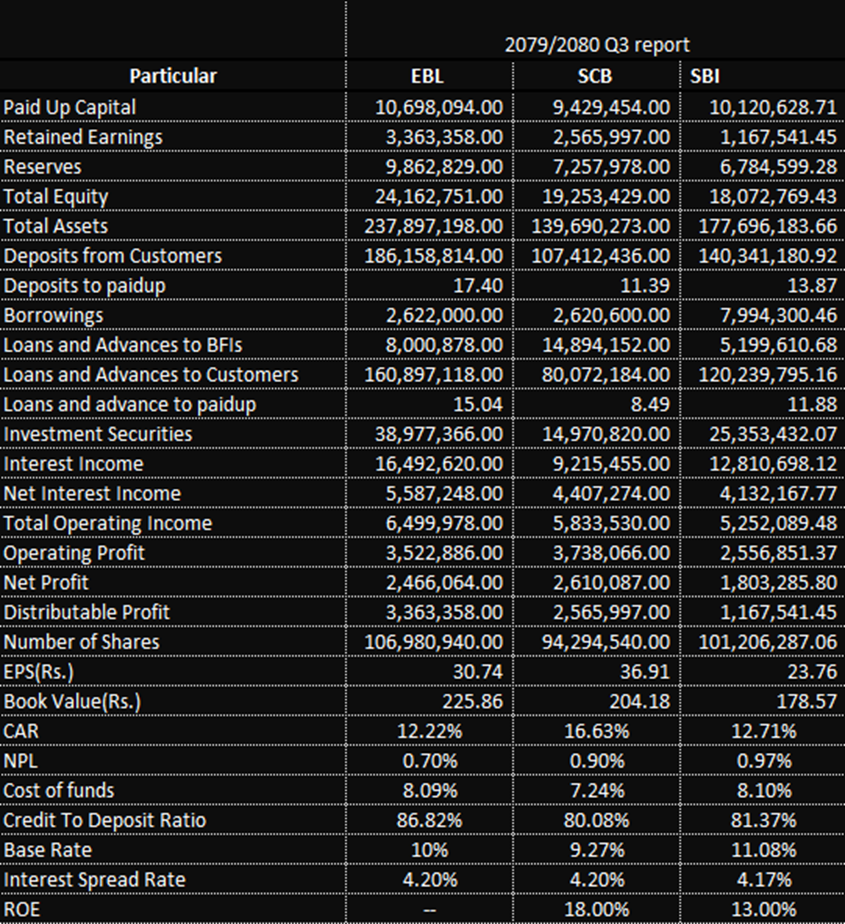

When analyzing the financial statements of banks to make well-informed investment decisions, it is important to consider the following metrics:

CASA Ratio: The CASA ratio represents the proportion of deposits held in current and savings accounts compared to total deposits. A higher CASA ratio indicates lower funding costs and increased profitability for banks. Banks with a high CASA ratio, such as SCB (49.38%), EBL (35.46%), and SBI (34.26%), are preferred options due to their lower cost of capital.

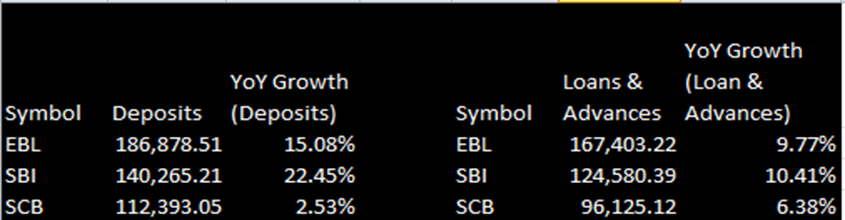

Deposit and Loan Growth: Examining deposit growth and the ratio of deposits to paid-up capital helps assess a bank's capacity to provide loans and its profitability. Banks with higher deposit growth, like SBI (22.45%), EBL (15.08%), and SCB (2.53%), are generally more profitable.

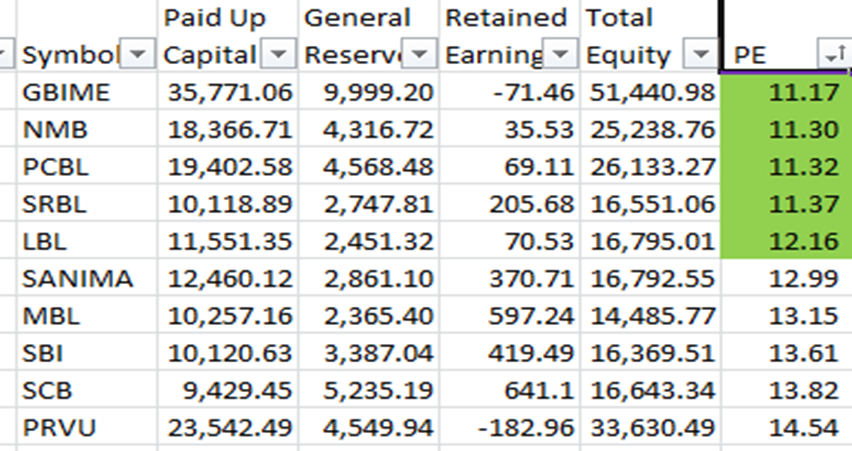

Capital Adequacy Ratio (CAR): The CAR measures a bank's financial buffer to absorb losses and protect depositors' funds. Banks with higher CAR, such as SCB (16.63%), SBI (12.71%), and EBL (12.22%), have greater capacity for loan extension and are preferable options.

Non-performing Loans (NPL): Low NPL ratios indicate healthier loan portfolios, prudent lending practices, and lower risk of defaults. Banks with low NPL ratios generate higher profits, maintain higher liquidity levels, and are viewed as more stable by investors.

Spread Rates: Banks are required to maintain a spread of 4%, except in cases of successful mergers where the spread rate may exceed by up to 1%. Adhering to spread rate regulations ensures stability and fairness within the banking sector.

Base Rate: Base rate represents the minimum lending rate for commercial banks. Lower base rates result in increased profitability, while higher rates have the opposite effect. Banks with lower base rates, like SCB (9.27%), EBL (10%), and SBI (11.08%), benefit from lower cost of capital and higher profitability.

Earnings per Share (EPS): EPS measures the profitability of a company and its capacity to distribute dividends. Banks with higher EPS, such as SCB (36.91), EBL (30.74), and SBI (23.76), indicate stronger financial performance.

Return on Equity (ROE): ROE measures a company's profitability and efficiency in generating profits from shareholders' equity. Higher ROE suggests effective utilization of equity capital and is favorable to investors.

Book Value: Book value indicates a bank's net worth and financial soundness. Higher book values are preferable when evaluating banks.

Dividend Capacity: Dividend capacity represents the proportion of profits that can be allocated to shareholders as dividends. Banks with higher dividend capacity, such as EBL (31%), SCB (27.21%), and SBI (11.53%), are considered more attractive to investors.

Considering these metrics helps investors assess the financial strength, profitability, and potential risks associated with investing in the banking sector.

Post a Comment